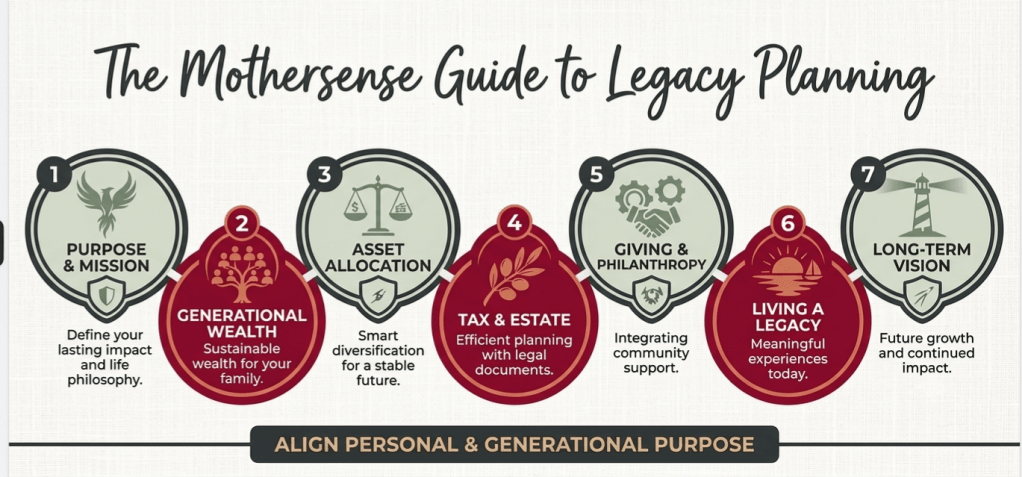

Life doesn’t happen in a vacuum. Between the long hauls on the road, the creative sparks at 2 AM, and the quiet moments at the kitchen table, we all need a plan. I have spent years learning how to protect what matters most—not because I love paperwork, but because I love my family.

After moving to an independent insurance model, I now have the freedom to shop around for you. I don’t work for one big company. I work for you. While my primary expertise is in Term Life and Final Expense, being independent means I have a wide range of options to fit almost any situation. If I don’t have the answer, I have the network to find it.

The Power Suite: Tools I Trust I am an Ambassador for these services because they solve the actual problems hard-working people face every day. I don’t recommend things I don’t believe in.

Legacy Promises Network Protecting your final story is the ultimate act of “Mothersense.” Whether you are looking at final expenses or securing your intellectual work, don’t leave your family guessing. This is about making promises today that they can rely on tomorrow.

My Debt Navigator In this economy, debt can feel like a weight you will never drop. I trust this navigator to help families find the most efficient path out of the red and back into the black. It is about taking the wheel of your financial future.

Let’s Connect for a Financial Check-up I still carry the knowledge of a deep Financial Needs Analysis. You might be looking for a budget-friendly Final Expense plan so your kids aren’t left with a bill, or maybe you just want to see if your current coverage is actually keeping up with inflation. Maybe even set up a plan to have a policy with living benefits and mortgage protection, let me know.

I am a Texas-based independent agent who understands the reality of the road and the rhythm of a busy home. Let’s sit down and see where you are. No judgment, just sense.

Life has a way of moving faster than our paperwork. We go through seasons—the “topsy-turvy” months where everything feels like it’s shifting under our feet. Maybe it’s a career change, a shift in the family dynamic, or just the realization that the “Second Half” of life is approaching faster than we thought. When things get messy, the first thing we usually neglect is the fine print. But here is the truth: Your intentions mean very little if your documentation is out of date. The Beneficiary Blindspot Think about the life insurance policy you bought years ago, or that old 401(k) from three jobs back. Who is the beneficiary? Is it an ex-partner? A parent who has passed on? A child who is now an adult? It’s not just about insurance. It’s your bank accounts, your retirement funds, and your legal titles. If the names on those documents don’t match your current reality, the state—not your heart—decides where your hard-earned legacy goes. Starting the “Awkward” Conversation I know why we wait. These conversations feel heavy. They feel like you’re inviting the “what-ifs” into the room. But I’ve learned that a moment of awkwardness is a small price to pay for a lifetime of protection. Whether you are looking at your first policy or realizing your current coverage is a “fiasco” that doesn’t fit your life anymore, the most important thing you can do is start. You don’t have to have all the answers; you just have to have the courage to ask the questions. You Don’t Have to Walk it Alone I’ve spent my life learning that resilience isn’t just about surviving the storm—it’s about building a sturdy house before the wind starts blowing. If you’re feeling bogged down or overwhelmed by where to begin, I can help. I can help you audit where you are, identify the gaps, and direct you to the right subject matter experts to ensure your family is shielded from the “what-ifs.” Let’s Secure Your “Second Half” Don’t let your legacy be decided by a document you forgot to update. Let’s have the conversation today so your family doesn’t have to have it during a crisis tomorrow

Julie Kilcrease Licensed Life Insurance Agent | Texas NPN: 21375920 Helping Texas families build a bridge to a secure second half.

I shared it without thinking twice. A GFM for my former father-in- law, and then, a friend of a friend. A family I didn’t know personally but recognized in the way you recognize anyone who looks like people you love. The photo was from a better day — a birthday, maybe, or a holiday. Everyone smiling. No one knowing what was coming. I hit share. I donated what I could. I scrolled on. And then I sat with it. Because here’s the thing nobody says out loud when those posts go around: A GoFundMe is not a plan. It’s what happens when there wasn’t one. I’ve been in this industry long enough to know what the aftermath looks like. Not the GoFundMe stage — the stage after that. When the campaign closes. When the casseroles stop coming. When the world moves on and that family is still sitting inside a life that financially collapsed overnight. The mortgage didn’t pause for grief. The utility companies didn’t send condolences. The kids still needed things. And the person who held it all together was gone. That’s the part that doesn’t make it into the fundraiser description. The slow, grinding weight of trying to rebuild a life when the foundation was pulled out from under you — with no parachute, no cushion, nothing but the kindness of strangers and a Donate button. I’m not here to scare you. I’m here because I’ve had the hard conversations — the ones that happen after it’s too late to do anything about it — and I would rather have an uncomfortable conversation with you now than a heartbreaking one later. This is what I do. Not because it’s a job, but because it matters in a way that is genuinely hard to explain until you’ve watched a family try to survive without it. There is a solution for where you are right now — whatever your budget, whatever your stage of life: Mortgage Protection — so your family keeps the roof over their heads, no matter what happens to you. Final Expense Coverage — so the people grieving you aren’t also drowning in bills they didn’t see coming. Living Benefits — so a diagnosis doesn’t also become a financial crisis while you’re still here fighting. You don’t have to have it all figured out. You just have to start. If you’re in Texas, I’d love to sit down with you and find something that actually fits your life and your budget — no pressure, no jargon, just an honest conversation. If you’re outside of Texas, I have trusted colleagues across the country and I will personally make sure you’re connected to someone who will take care of you. Your family deserves more than a Donate button. Let’s build something that holds. Drop a comment or send me a message. Let’s talk

The Dinner Table Conversation We Avoid… But Shouldn’t There’s something sacred about the dinner table. It’s where backpacks get unpacked, where stories spill out about teachers and tests, where we remind our kids to eat their vegetables and ask about their day. It’s where life happens. Messy, loud, beautiful life. Between the “Did you finish your homework?” and “Don’t forget practice tomorrow,” we’re building something bigger than routines. We’re building a sense of safety.

But here’s a question most of us never ask in those moments: What would happen to all of this if I wasn’t here tomorrow?

Peace of Mind Isn’t Just a Feeling. It’s a Plan. We spend so much time protecting our families in everyday ways. Locking doors, checking grades, making sure everyone gets where they need to be.

But real peace of mind comes from knowing your family wouldn’t be left overwhelmed, confused, or struggling to pick up the pieces if the unthinkable happened. Grief is hard enough without paperwork, court dates, and unanswered questions.

A Conversation I’ve Already Started I’ll be honest. I’ve had these conversations with my family. I have a document ready with all my important logins and passwords, and I keep it updated regularly. Someone knows where it is. That matters more than people realize. I’ve talked through the hard things with my husband and my older kids. Not because I want to, but because I need to. And yes, sometimes it gets uncomfortable.

Like when I told my kids I changed my mind about insisting on cremation. I told them, “Do what you guys want.” There are five of them, so good luck with that decision. But I did give them one non negotiable. At whatever kind of gathering they have for me, they must play “Good Riddance (Time of Your Life).” (They don’t need to know how it ties back to an episode of ER I watched with my mom that left us both bawling.)

My youngest gets so uncomfortable every time I bring it up. He tells me, “Mom, tell the others, not me.”

Oh, I do!

I tell all of them. Often enough to make sure they know. Because As Much As It Sucks, It’s Necessary I know this isn’t a fun topic. It sucks. But it is necessary. If I leave this world suddenly, I don’t want my family sitting around asking:

What do we do now?

Where is everything?

What would she have wanted?

I cannot be here forever with them. But I can guide them through these choices now. We all die. That is the truth no one likes to say out loud. But I can ease some of the frustration, some of the confusion, and even a little of the pain that comes after.

I can declutter my own things, so they don’t have to. I can give them sentimental gifts while I am still around to know they enjoy them.

The Reality Most Families Aren’t Prepared For:

Without preparation, families are left trying to figure everything out while grieving:

Where are the bank accounts? Who gets access to what? What were the wishes? How do they even begin?

If things are not set up properly, it can all end up in probate. This is a long, expensive, and emotionally draining process. Just ask my sister. We learned the hard way. And it does not have to be that way. Simple Steps That Change Everything

This is not about fear. It is about love. These are simple, practical ways to protect your family:

✔️ Financial Protection Have life insurance or burial coverage Consider prepaid funeral plans ✔️ Direct Beneficiaries Make sure all bank accounts have designated beneficiaries This allows access with just an ID and death certificate ✔️ Protect Your Home

File a Transfer on Death (TOD) deed

This helps your home pass directly to your chosen person without probate The Documents That Speak for You When You Can’t Putting your wishes in writing is one of the greatest gifts you can leave behind:

Living Will outlines your healthcare wishes

Durable Power of Attorney handles legal decisions

Healthcare Power of Attorney handles medical decisions

Last Will and Testament determines who receives your belongings

Funeral Planning Declaration states your final wishes

These do not have to be complicated. They just need to clearly reflect your wishes.

Make It Easy for the People You Love One of the most overlooked steps is also one of the most important. Create a master list of:

Bank accounts

Investments

Credit cards

Bills and utilities

Make sure someone knows: Where your life insurance policies are Where to find titles for vehicles and property How to access your accounts and passwords

Because in today’s world, access is everything.

The Conversation That Matters Most

Talk to your family. Even when it feels awkward. Even when they do not want to hear it. Tell them your wishes. Explain your decisions. Let them ask questions. What feels uncomfortable now becomes clarity later. It’s Not About the End. It’s About Love. We cannot control what happens tomorrow. But we can control how prepared we are today. So maybe tonight, between dinner and dishes, you start a different kind of conversation. Not a scary one. A loving one. Because true peace of mind is not just knowing your family is okay today. It is knowing they will be okay no matter what.

Love and light! 😉

I write this not to be a sales person, I write it because I have LIVED IT, and I have seen up close too many loved ones left grieving with no plan to follow. It matters.

Start the Year Right: A Financial Check-Up and Planning for the Unexpected

As January is flying by, it’s a great time to hit the refresh button on many aspects of your life—your finances included. While it’s easy to get caught up in the excitement of New Year’s resolutions and personal goals, one of the most important things you can do at the start of the year is ensure that your financial and legal documents are in order. Doing a financial check-up and reviewing critical documents may not be the most thrilling task, but it can save your family from unnecessary stress and confusion should something happen to you or your spouse.

1. Perform a Financial Check-Up

Start by reviewing your financial situation:

Review your budget and spending habits: Are you living within your means? Have your financial goals changed? It’s important to adjust your budget to reflect your current priorities, whether that’s saving for a major purchase, paying off debt, or investing in retirement.

Check your credit report: Get a copy of your credit report to ensure there are no errors or signs of identity theft. Correcting mistakes early can save you a lot of headaches down the line.

Evaluate your emergency savings: Ideally, you should have 3-6 months of living expenses saved up in case of unexpected emergencies. If this isn’t the case, make it a priority this year to build or replenish your emergency fund.

Revisit retirement and investment accounts: Check in on the performance of your retirement accounts and investment portfolios. Make sure your contributions align with your goals and, if necessary, adjust your asset allocation based on your risk tolerance and time horizon.

2. Update Your Will and Trust

Many people put off creating a will or updating it because it can feel morbid or overwhelming. However, it’s a crucial step in ensuring your assets are distributed according to your wishes and that your family members are taken care of. If your circumstances have changed—perhaps you’ve acquired new assets, had a child, or experienced a life event like a marriage or divorce—be sure to revise your will to reflect these changes. You may also want to consider setting up a trust to avoid probate and streamline the transfer of assets.

3. Review Beneficiaries for Insurance and Bank Accounts

It’s not uncommon for people to forget to update their beneficiary designations on life insurance policies, retirement accounts (like 401(k)s or IRAs), and even bank accounts. If you’ve had any life changes—such as a marriage, divorce, or the birth of a child—this should be a top priority. Ensure that the beneficiaries listed reflect your current wishes and that your loved ones will be taken care of in the event of your death.

4. Set Up Power of Attorney

A Power of Attorney (POA) is a legal document that designates someone to make financial decisions on your behalf if you’re unable to do so yourself due to illness, injury, or incapacitation. Having a trusted person in place who can handle financial matters for you is essential to ensure your financial obligations are met during a difficult time. You can also set up a Healthcare Power of Attorney to appoint someone to make medical decisions on your behalf if you’re unable to communicate those decisions yourself.

5. Create Advance Directives

An advance directive (also known as a living will) outlines your preferences for medical care should you be in a position where you cannot express your wishes. This can include instructions for life-sustaining treatment, organ donation, and other aspects of end-of-life care. Many people shy away from thinking about these situations, but having clear, legally recognized instructions can relieve your loved ones of difficult decisions during emotionally charged times. Make sure your advance directives are signed, dated, and stored in a place where your family can easily access them.

6. Organize Your Documents and Make Things Easy for Your Family

Beyond the legal documents and financial accounts, consider organizing important information for your family. Create a document or folder where you record all necessary details about your accounts, passwords, insurance policies, and any other key information that your family members may need in the event of an emergency or your passing. Include things like:

Where you keep physical documents

Account numbers, login details, and passwords (using a password manager is a secure option)

Insurance policies, including life, home, auto, and health

Contact information for professionals (lawyers, accountants, financial advisors)

While it might seem like a lot of work upfront, taking the time to get your affairs in order now can provide peace of mind for both you and your loved ones.

7. Talk to Your Family About Your Wishes

Beyond the paperwork, it’s crucial to have an open and honest conversation with your family about your wishes. This includes discussing things like your preferences for healthcare, your end-of-life care decisions (such as a Do Not Resuscitate or DNR order), and what you want to happen with your possessions. While it may feel uncomfortable, leaving these things unspoken can lead to confusion, stress, and even family conflict when emotions run high.

The Importance of Doing the Work

It may seem daunting to go through this process, but it’s far better to address these matters now than leave your family to guess your intentions. If you were to fall ill or unexpectedly pass away, having these legal and financial arrangements in place would ensure that your family isn’t left scrambling, unsure of your wishes, or dealing with unnecessary administrative headaches. It’s not about being morbid—it’s about being proactive and ensuring that your loved ones have clarity and peace of mind when they need it most.

This year, make it a priority to set aside time for your financial and legal check-up. You’ll feel better knowing that you’ve taken steps to protect your family and their future.